Portfolio Risk Management during 2008 Financial Crisis

GitHub Project

A project on portfolio risk management considering returns of four major investment banks during financial crisis (2008-2010) using Python.

Stocks of following companies were taken in a portfolio:

1. Goldman Sachs

2. Citi

3. Morgan Stanley

4. JPMorgan Chase & Co.

Working involves following modules:

1. Portfolio risk measures (VaR and CVaR) with varying confidence intervals.

2. Risk estimation techniques - Parametric, Historical and Monte Carlo Simulation.

3. Modern Portfolio Theory (Efficient Portfolio and Efficient Frontiers).

4. Optimizing portfolio weights with an objective function to reduce CVaR loss.

Let’s dive into the code.

Importing Python Packages

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

import plotly.graph_objects as go

import statsmodels.api as sm

from pypfopt import CLA

from pypfopt.expected_returns import mean_historical_return

from pypfopt.risk_models import CovarianceShrinkage

from scipy.stats import norm

from scipy.stats import norm,anderson

from scipy.stats import skewnorm, skewtest

import seaborn as sns

from matplotlib import style

Data contains daily stock prices of 4 major banks(Morgan Stanley, Citi, JPMorgan Chase, Goldman Sachs) during period before, during and after Financial Crisis of 2008

df1 = pd.read_csv("Financial_Stocks.csv")

df = df1.copy()

Data Preprocessing

df.head(10)

| Date | Close_MS | Close_Citi | JPM_Close | GS_Close | |

|---|---|---|---|---|---|

| 0 | 03-01-2007 | 81.620003 | 552.500000 | 48.070000 | 200.720001 |

| 1 | 04-01-2007 | 81.910004 | 550.599976 | 48.189999 | 198.850006 |

| 2 | 05-01-2007 | 80.860001 | 547.700012 | 47.790001 | 199.050003 |

| 3 | 08-01-2007 | 81.349998 | 550.500000 | 47.950001 | 203.729996 |

| 4 | 09-01-2007 | 81.160004 | 545.700012 | 47.750000 | 204.080002 |

| 5 | 10-01-2007 | 81.570000 | 541.299988 | 48.099998 | 208.110001 |

| 6 | 11-01-2007 | 82.370003 | 541.700012 | 48.310001 | 211.880005 |

| 7 | 12-01-2007 | 82.860001 | 543.799988 | 47.990002 | 213.990005 |

| 8 | 16-01-2007 | 82.610001 | 547.700012 | 48.389999 | 213.589996 |

| 9 | 17-01-2007 | 82.379997 | 543.900024 | 48.430000 | 213.229996 |

df.isna().sum()

Date 0

Close_MS 0

Close_Citi 0

JPM_Close 0

GS_Close 0

dtype: int64

df['Date'] = pd.to_datetime(df['Date'])

df = df.set_index('Date')

df4 = df.copy()

df.head(3)

| Close_MS | Close_Citi | JPM_Close | GS_Close | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | 81.620003 | 552.500000 | 48.070000 | 200.720001 |

| 2007-04-01 | 81.910004 | 550.599976 | 48.189999 | 198.850006 |

| 2007-05-01 | 80.860001 | 547.700012 | 47.790001 | 199.050003 |

Below Summary explains high volatility of each stock during the time of crisis

df.describe()

| Close_MS | Close_Citi | JPM_Close | GS_Close | |

|---|---|---|---|---|

| count | 1007.000000 | 1007.000000 | 1007.000000 | 1007.000000 |

| mean | 40.228898 | 186.092056 | 40.848590 | 164.917607 |

| std | 20.498821 | 185.851510 | 6.746547 | 40.236383 |

| min | 9.200000 | 10.200000 | 15.900000 | 52.000000 |

| 25% | 26.000000 | 39.099998 | 37.730002 | 144.930001 |

| 50% | 30.790001 | 65.199997 | 41.529999 | 166.750000 |

| 75% | 49.979999 | 292.550003 | 45.330000 | 190.285004 |

| max | 89.300003 | 552.500000 | 53.200001 | 247.919998 |

# from 2007 - 2010

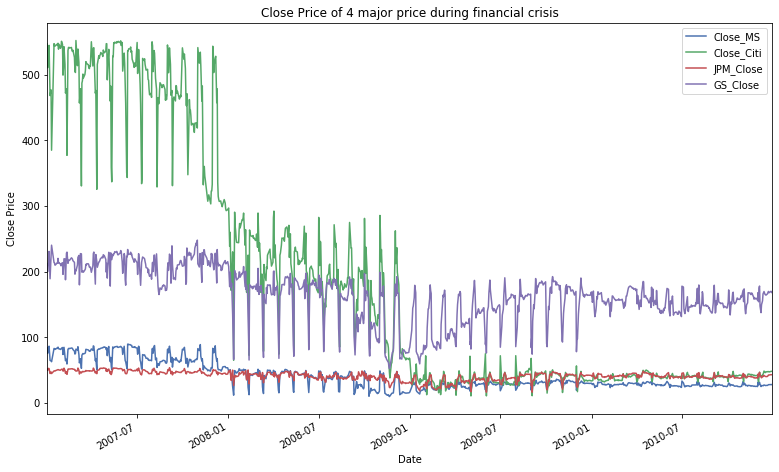

df.plot(legend = 'MS',figsize=(13,8))

plt.ylabel("Close Price")

plt.title('Close Price of 4 major price during financial crisis')

Text(0.5, 1.0, 'Close Price of 4 major price during financial crisis')

Quantifying Return (Taking log returns in place of close prices due to high autocorrelation in prices)

df['Lag_MS'] = df['Close_MS'].shift(1)

df['Return_MS'] = (np.log(df['Close_MS']/df['Lag_MS']))*100

df['Lag_Citi'] = df['Close_Citi'].shift(1)

df['Return_Citi'] = (np.log(df['Close_Citi']/df['Lag_Citi']))*100

df['Lag_JPM'] = df['JPM_Close'].shift(1)

df['Return_JPM'] = (np.log(df['JPM_Close']/df['Lag_JPM']))*100

df['Lag_GS'] = df['GS_Close'].shift(1)

df['Return_GS'] = (np.log(df['GS_Close']/df['Lag_GS']))*100

df1 = df.drop(['Lag_Citi','Lag_MS','Lag_JPM','Lag_GS'],axis=1)

df2 = df1.drop(['Close_MS','Close_Citi','GS_Close','JPM_Close'],axis=1)

df3 = df2.copy()

df3.head(10)

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | NaN | NaN | NaN | NaN |

| 2007-04-01 | 0.354677 | -0.344488 | 0.249323 | -0.936011 |

| 2007-05-01 | -1.290186 | -0.528084 | -0.833508 | 0.100526 |

| 2007-08-01 | 0.604153 | 0.509924 | 0.334239 | 2.323950 |

| 2007-09-01 | -0.233824 | -0.875756 | -0.417976 | 0.171652 |

| 2007-10-01 | 0.503898 | -0.809576 | 0.730307 | 1.955471 |

| 2007-11-01 | 0.975978 | 0.073873 | 0.435646 | 1.795331 |

| 2007-12-01 | 0.593112 | 0.386915 | -0.664590 | 0.990921 |

| 2007-01-16 | -0.302170 | 0.714620 | 0.830046 | -0.187104 |

| 2007-01-17 | -0.278810 | -0.696226 | 0.082630 | -0.168689 |

df3.describe()

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| count | 1006.000000 | 1006.000000 | 1006.000000 | 1006.000000 |

| mean | -0.108756 | -0.243700 | -0.012875 | -0.017902 |

| std | 5.008769 | 5.580447 | 3.865965 | 3.441285 |

| min | -29.965820 | -49.469624 | -23.227805 | -21.022262 |

| 25% | -1.735934 | -1.991310 | -1.498332 | -1.418094 |

| 50% | -0.043817 | -0.203060 | -0.072195 | -0.054054 |

| 75% | 1.598136 | 1.576655 | 1.400192 | 1.556280 |

| max | 62.585004 | 45.631619 | 22.391712 | 23.481773 |

sns.set(style="whitegrid")

# #plt.figure(figsize=(20, 12))

# plt.xlabel('LogReturn')

# style.use('ggplot')

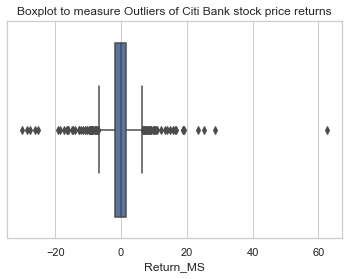

sns.boxplot(x=df3['Return_MS'])

plt.title('Boxplot to measure Outliers of Citi Bank stock price returns')

Text(0.5, 1.0, 'Boxplot to measure Outliers of Citi Bank stock price returns')

sns.set(style="whitegrid")

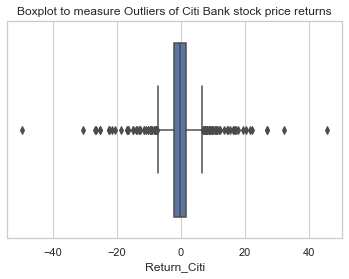

sns.boxplot(x=df3['Return_Citi'])

plt.title('Boxplot to measure Outliers of Citi Bank stock price returns')

Text(0.5, 1.0, 'Boxplot to measure Outliers of Citi Bank stock price returns')

sns.set(style="whitegrid")

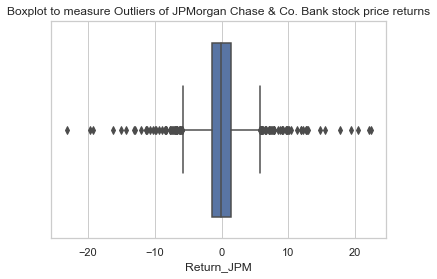

sns.boxplot(x=df3['Return_JPM'])

plt.title('Boxplot to measure Outliers of JPMorgan Chase & Co. Bank stock price returns')

Text(0.5, 1.0, 'Boxplot to measure Outliers of JPMorgan Chase & Co. Bank stock price returns')

sns.set(style="whitegrid")

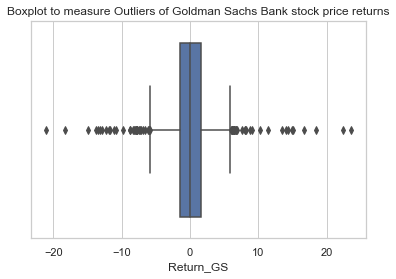

sns.boxplot(x=df3['Return_GS'])

plt.title('Boxplot to measure Outliers of Goldman Sachs Bank stock price returns')

Text(0.5, 1.0, 'Boxplot to measure Outliers of Goldman Sachs Bank stock price returns')

Considering equal weightage to each asset in a portfolio

returns = df3.dropna(axis=0)

Allocation of 25% of our Investment in each of the security

w = (0.25,0.25,0.25,0.25)

# Multilying weight vector with returns vector to calculate portfolio returns

portfolio_returns = returns.dot(w)

portfolio_returns.head(10)

Date

2007-04-01 -0.169125

2007-05-01 -0.637813

2007-08-01 0.943067

2007-09-01 -0.338976

2007-10-01 0.595025

2007-11-01 0.820207

2007-12-01 0.326589

2007-01-16 0.263848

2007-01-17 -0.265274

2007-01-18 -0.922285

dtype: float64

losses = -1*portfolio_returns

losses.head(10)

Date

2007-04-01 0.169125

2007-05-01 0.637813

2007-08-01 -0.943067

2007-09-01 0.338976

2007-10-01 -0.595025

2007-11-01 -0.820207

2007-12-01 -0.326589

2007-01-16 -0.263848

2007-01-17 0.265274

2007-01-18 0.922285

dtype: float64

-ve returns are losses and +ve returns a are profit

Pandas Series Object to Pandas Dataframe

portfolio_returns_new = pd.Series(portfolio_returns)

print (portfolio_returns_new)

Date

2007-04-01 -0.169125

2007-05-01 -0.637813

2007-08-01 0.943067

2007-09-01 -0.338976

2007-10-01 0.595025

...

2010-12-23 -0.600600

2010-12-27 1.245777

2010-12-28 0.058732

2010-12-29 -0.776881

2010-12-30 -0.082041

Length: 1006, dtype: float64

df = portfolio_returns_new.to_frame()

df = df.rename(columns={0: "returns"})

df.head(10)

| returns | |

|---|---|

| Date | |

| 2007-04-01 | -0.169125 |

| 2007-05-01 | -0.637813 |

| 2007-08-01 | 0.943067 |

| 2007-09-01 | -0.338976 |

| 2007-10-01 | 0.595025 |

| 2007-11-01 | 0.820207 |

| 2007-12-01 | 0.326589 |

| 2007-01-16 | 0.263848 |

| 2007-01-17 | -0.265274 |

| 2007-01-18 | -0.922285 |

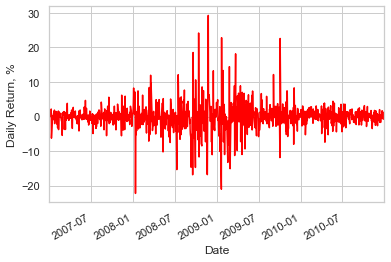

portfolio_returns.plot(color='red').set_ylabel("Daily Return, %")

plt.show()

Above graph shows very high volatility from July 2008 to July 2009

The asset prices plot shows how the global financial crisis created a loss in confidence in investment banks from September 2008 There was an event during September that precipitated this decline. The ‘spikiness’ of portfolio returns indicates how uncertain and volatile asset returns became.

portfolio_returns_percent = portfolio_returns*100

VaR using Variance Covariance (Parametric Estimation)

The parametric method, also known as the variance-covariance method, is a risk management technique for calculating the value at risk (VaR) of a portfolio of assets. The value at risk is a statistical risk management technique measuring the maximum loss that an investment portfolio is likely to face within a specified time frame with a certain degree of confidence. The variance-covariance method used to calculate the value at risk identifies the mean, or expected value, and standard deviation of an investment portfolio.

covar = df3.cov()

Correlation in Percentage

print(covar)

Return_MS Return_Citi Return_JPM Return_GS

Return_MS 25.087771 16.949962 12.411611 13.923230

Return_Citi 16.949962 31.141387 15.314959 12.128333

Return_JPM 12.411611 15.314959 14.945687 9.666014

Return_GS 13.923230 12.128333 9.666014 11.842443

# Annualize the covariance using 252 trading days per year

covar_ann = covar*252

print(covar_ann)

Return_MS Return_Citi Return_JPM Return_GS

Return_MS 6322.118322 4271.390381 3127.726038 3508.654003

Return_Citi 4271.390381 7847.629460 3859.369779 3056.339857

Return_JPM 3127.726038 3859.369779 3766.313007 2435.835409

Return_GS 3508.654003 3056.339857 2435.835409 2984.295634

portfolio_variance = np.transpose(w)@covar_ann@w

portfolio_volatility = np.sqrt(portfolio_variance)

Annual Portfolio Volatliltiy of 61%

The volatility of a portfolio of stocks is a measure of how wildly the total value of all the stocks in that portfolio appreciates or declines.

print(portfolio_volatility)

61.96722286680826

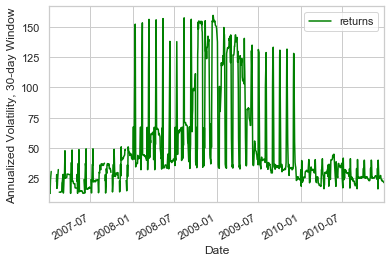

30 Day Rolling Volatility

windowed = df.rolling(30)

volatility = windowed.std()*np.sqrt(252)

volatility.plot(color = 'green').set_ylabel("Annualized Volatility, 30-day Window")

Text(0, 0.5, 'Annualized Volatility, 30-day Window')

df.head(10)

| returns | |

|---|---|

| Date | |

| 2007-04-01 | -0.169125 |

| 2007-05-01 | -0.637813 |

| 2007-08-01 | 0.943067 |

| 2007-09-01 | -0.338976 |

| 2007-10-01 | 0.595025 |

| 2007-11-01 | 0.820207 |

| 2007-12-01 | 0.326589 |

| 2007-01-16 | 0.263848 |

| 2007-01-17 | -0.265274 |

| 2007-01-18 | -0.922285 |

Risk Factors

Variables or events that drive portfolio return and volatility

Two types of risk factors are: 1. Systematic Risk 2. Idisyncratic Risk

Systematic Risk

Systematic risk is inherent to the market as a whole, reflecting the impact of economic, geo-political and financial factors. This type of risk is distinguished from unsystematic risk, which impacts a specific industry or security. Investors can somewhat mitigate the impact of systematic risk by building a diversified portfolio. Ex: interest rate changes, inflation, recessions, and wars, among other major changes.

Idiosyncratic Risk

Idiosyncratic risk refers to the inherent factors that can negatively impact individual securities or a very specific group of assets. The opposite of Idiosyncratic risk is a systematic risk, which refers to broader trends that impact the overall financial system or a very broad market. Idiosyncratic risk can generally be mitigated in an investment portfolio through the use of diversification Idiosyncratic risk is a type of investment risk that is endemic to an individual asset (like a particular company’s stock), or a group of assets (like a particular sector’s stocks), or in some cases, a very specific asset class (like collateralized mortgage obligations).

Idiosyncratic Risk vs. Systematic Risk

While idiosyncratic risk is, by definition, irregular and unpredictable, studying a company or industry can help an investor to identify and anticipate—in a general way—its idiosyncratic risks. Idiosyncratic risk is also highly individual, even unique in some cases. It can, therefore, be substantially mitigated or eliminated from a portfolio by using adequate diversification. Proper asset allocation, along with hedging strategies, can minimize its negative impact on an investment portfolio by diversification or hedging. In contrast, systematic risk cannot be mitigated just by adding more assets to an investment portfolio. This market risk cannot be eliminated by adding stocks of various sectors to one’s holdings. These broader types of risk reflect the macroeconomic factors that affect not just a single asset but other assets like it and greater markets and economies as well.

Factor Models

Factor models assess on which risk factors asset returns or volatility are mostly dependent. We can model theses factors using : 1. Ordinary Least Square - Regression Model - dependent variable - Asset returns/volatility independent variable - risk factors 2. Fama French Model - combination of market risk and idiosyncratic risk (firm size and value)

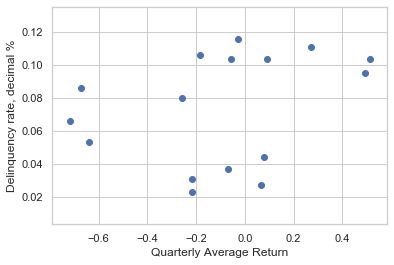

Considering MBS(Mortgage Backed Security) 90 days mortgage Delinquency as a risk factor which caused the bankcruptcy of Lehman Brothers. Risk factor delinquency rate was highly correlated with the returns.

Risk factor models often rely upon data that is of different frequencies. A typical example is when using quarterly macroeconomic data, such as prices, unemployment rates. here also delinquency rate is taken for 90 days (1 Q) so sampling returns for quarter

returns_avg = df.resample('Q').mean()

returns_avg.tail()

| returns | |

|---|---|

| Date | |

| 2009-12-31 | -0.028065 |

| 2010-03-31 | 0.269598 |

| 2010-06-30 | -0.182155 |

| 2010-09-30 | 0.090613 |

| 2010-12-31 | -0.056955 |

# Now convert daily returns to weekly minimum returns

returns_min = df.resample('Q').min()

returns_min.head()

| returns | |

|---|---|

| Date | |

| 2007-03-31 | -6.233800 |

| 2007-06-30 | -4.161445 |

| 2007-09-30 | -5.513566 |

| 2007-12-31 | -5.545354 |

| 2008-03-31 | -22.216434 |

delin = pd.read_csv("Delinq_rate.csv")

returns_avg.describe()

| returns | |

|---|---|

| count | 16.000000 |

| mean | -0.097230 |

| std | 0.367616 |

| min | -0.718012 |

| 25% | -0.228185 |

| 50% | -0.064064 |

| 75% | 0.082071 |

| max | 0.512064 |

delin.describe()

| Delinq_Rate | |

|---|---|

| count | 16.000000 |

| mean | 0.073975 |

| std | 0.033431 |

| min | 0.023100 |

| 25% | 0.042025 |

| 50% | 0.082700 |

| 75% | 0.103525 |

| max | 0.115400 |

plt.scatter(returns_avg,delin['Delinq_Rate'])

plt.xlabel("Quarterly Average Return")

plt.ylabel("Delinquency rate, decimal %")

Text(0, 0.5, 'Delinquency rate, decimal %')

plt.scatter(returns_min,delin['Delinq_Rate'])

plt.xlabel("Quarterly Min Return")

plt.ylabel("Delinquency rate, decimal %")

Text(0, 0.5, 'Delinquency rate, decimal %')

Initial assessment indicates that there is little correlation between average returns and mortgage delinquencies, but a stronger negative correlation exists between minimum returns and delinquency. In the following exercises we’ll quantify this using least-squares regression.

delin.head()

| Date | Delinq_Rate | |

|---|---|---|

| 0 | 31-03-2007 | 0.0231 |

| 1 | 30-06-2007 | 0.0271 |

| 2 | 30-09-2007 | 0.0309 |

| 3 | 31-12-2007 | 0.0367 |

| 4 | 31-03-2008 | 0.0438 |

delin['Date'] = pd.to_datetime(delin['Date'])

delin = delin.set_index('Date')

delin.head()

| Delinq_Rate | |

|---|---|

| Date | |

| 2007-03-31 | 0.0231 |

| 2007-06-30 | 0.0271 |

| 2007-09-30 | 0.0309 |

| 2007-12-31 | 0.0367 |

| 2008-03-31 | 0.0438 |

regression = sm.OLS(returns_avg,delin['Delinq_Rate']).fit()

print(regression.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: returns R-squared (uncentered): 0.015

Model: OLS Adj. R-squared (uncentered): -0.051

Method: Least Squares F-statistic: 0.2271

Date: Sat, 25 Jul 2020 Prob (F-statistic): 0.641

Time: 08:04:12 Log-Likelihood: -6.6308

No. Observations: 16 AIC: 15.26

Df Residuals: 15 BIC: 16.03

Df Model: 1

Covariance Type: nonrobust

===============================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------

Delinq_Rate -0.5580 1.171 -0.476 0.641 -3.054 1.938

==============================================================================

Omnibus: 0.056 Durbin-Watson: 1.468

Prob(Omnibus): 0.973 Jarque-Bera (JB): 0.252

Skew: -0.099 Prob(JB): 0.882

Kurtosis: 2.417 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

C:\Users\TAN\Anaconda3\lib\site-packages\scipy\stats\stats.py:1535: UserWarning:

kurtosistest only valid for n>=20 ... continuing anyway, n=16

regression_qmin = sm.OLS(returns_min,delin['Delinq_Rate']).fit()

print(regression_qmin.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: returns R-squared (uncentered): 0.594

Model: OLS Adj. R-squared (uncentered): 0.567

Method: Least Squares F-statistic: 21.92

Date: Sat, 25 Jul 2020 Prob (F-statistic): 0.000295

Time: 08:04:15 Log-Likelihood: -54.585

No. Observations: 16 AIC: 111.2

Df Residuals: 15 BIC: 111.9

Df Model: 1

Covariance Type: nonrobust

===============================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------

Delinq_Rate -109.8156 23.454 -4.682 0.000 -159.808 -59.824

==============================================================================

Omnibus: 0.853 Durbin-Watson: 0.828

Prob(Omnibus): 0.653 Jarque-Bera (JB): 0.718

Skew: -0.452 Prob(JB): 0.698

Kurtosis: 2.489 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

# Now convert daily returns to weekly minimum returns

returns_vol = df.resample('Q').std()

returns_vol.head()

| returns | |

|---|---|

| Date | |

| 2007-03-31 | 1.787018 |

| 2007-06-30 | 1.434462 |

| 2007-09-30 | 1.909144 |

| 2007-12-31 | 2.157466 |

| 2008-03-31 | 4.694626 |

regression_vol = sm.OLS(returns_vol,delin['Delinq_Rate']).fit()

print(regression_vol.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: returns R-squared (uncentered): 0.657

Model: OLS Adj. R-squared (uncentered): 0.634

Method: Least Squares F-statistic: 28.68

Date: Sat, 25 Jul 2020 Prob (F-statistic): 8.01e-05

Time: 08:04:18 Log-Likelihood: -35.971

No. Observations: 16 AIC: 73.94

Df Residuals: 15 BIC: 74.71

Df Model: 1

Covariance Type: nonrobust

===============================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------

Delinq_Rate 39.2452 7.328 5.356 0.000 23.627 54.864

==============================================================================

Omnibus: 1.168 Durbin-Watson: 0.517

Prob(Omnibus): 0.558 Jarque-Bera (JB): 0.832

Skew: 0.215 Prob(JB): 0.660

Kurtosis: 1.969 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

As seen from the regressions, mortgage delinquencies are acting as a systematic risk factor for both minimum quarterly returns and average volatility of returns, but not for average quarterly returns. The R-squared goodness of fit isn’t high in any case, but a model with more factors would likely generate greater explanatory power.

R-Squared is a statistical measure of fit that indicates how much variation of a dependent variable is explained by the independent variable(s) in a regression model.

Modern Portfolio Theory

What maximum return an investor can expect as per given risk apetite calculated from the portfolio volatility

Eficient Portfolio

portfolio with weights generating highest expected return for given level of risk

Efficient Frontier

Locus of (risk,return) pairs created by efficient portfolio

# pip install pyportfolioopt

# Compute the annualized average historical return

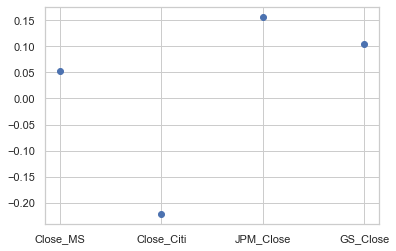

mean_returns = mean_historical_return(df4, frequency = 252)

# Plot the annualized average historical return

plt.plot(mean_returns, linestyle = 'None', marker = 'o')

plt.show()

mean_returns.head()

Close_MS 0.051932

Close_Citi -0.222364

JPM_Close 0.156725

GS_Close 0.104710

dtype: float64

The average historical return is usually available as a proxy for expected returns, but is not always accurate–a more thorough estimate of expected returns requires an assumption about the return distribution, which we’ll discuss in the context of Loss Distributions later in the course.

df4.head(10)

| Close_MS | Close_Citi | JPM_Close | GS_Close | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | 81.620003 | 552.500000 | 48.070000 | 200.720001 |

| 2007-04-01 | 81.910004 | 550.599976 | 48.189999 | 198.850006 |

| 2007-05-01 | 80.860001 | 547.700012 | 47.790001 | 199.050003 |

| 2007-08-01 | 81.349998 | 550.500000 | 47.950001 | 203.729996 |

| 2007-09-01 | 81.160004 | 545.700012 | 47.750000 | 204.080002 |

| 2007-10-01 | 81.570000 | 541.299988 | 48.099998 | 208.110001 |

| 2007-11-01 | 82.370003 | 541.700012 | 48.310001 | 211.880005 |

| 2007-12-01 | 82.860001 | 543.799988 | 47.990002 | 213.990005 |

| 2007-01-16 | 82.610001 | 547.700012 | 48.389999 | 213.589996 |

| 2007-01-17 | 82.379997 | 543.900024 | 48.430000 | 213.229996 |

# Import the CovarianceShrinkage object, it reduces/shrinks the errors/residuals while calculating the covariance matrix

# Create the CovarianceShrinkage instance variable

cs = CovarianceShrinkage(df4)

# Difference in calculating covariance matrix through covariance shrinkage and through sample cov() method

# Compute the sample covariance matrix of returns

sample_cov = df4.pct_change().cov() * 252

# Compute the efficient covariance matrix of returns

e_cov = cs.ledoit_wolf()

# Display both the sample covariance_matrix and the efficient e_cov estimate

print("Sample Covariance Matrix\n", sample_cov, "\n")

print("Efficient Covariance Matrix\n", e_cov, "\n")

Sample Covariance Matrix

Close_MS Close_Citi JPM_Close GS_Close

Close_MS 0.717102 0.450956 0.319404 0.372737

Close_Citi 0.450956 0.796039 0.398215 0.320531

JPM_Close 0.319404 0.398215 0.384847 0.247412

GS_Close 0.372737 0.320531 0.247412 0.304432

Efficient Covariance Matrix

Close_MS Close_Citi JPM_Close GS_Close

Close_MS 0.707324 0.425953 0.301695 0.352071

Close_Citi 0.425953 0.781884 0.376136 0.302760

JPM_Close 0.301695 0.376136 0.393490 0.233695

GS_Close 0.352071 0.302760 0.233695 0.317534

Although the differences between the sample covariance and the efficient covariance (found by shrinking errors) may seem small, they have a huge impact on estimation of the optimal portfolio weights and the generation of the efficient frontier. Practitioners generally use some form of efficient covariance for Modern Portfolio Theory.

# Create a dictionary of time periods (or 'epochs')

epochs = { 'during' : {'start': '1-1-2007', 'end': '31-12-2008'},

'after' : {'start': '1-1-2009', 'end': '31-12-2010'}

}

# Compute the efficient covariance for each epoch

e_cov = {}

for x in epochs.keys():

sub_price = df4.loc[epochs[x]['start']:epochs[x]['end']]

e_cov[x] = CovarianceShrinkage(sub_price).ledoit_wolf()

# Display the efficient covariance matrices for all epochs

print("Efficient Covariance Matrices\n", e_cov)

Efficient Covariance Matrices

{'during': Close_MS Close_Citi JPM_Close GS_Close

Close_MS 0.994390 0.465336 0.298613 0.434874

Close_Citi 0.465336 0.713035 0.364848 0.323977

JPM_Close 0.298613 0.364848 0.422516 0.224668

GS_Close 0.434874 0.323977 0.224668 0.408773, 'after': Close_MS Close_Citi JPM_Close GS_Close

Close_MS 0.388839 0.344939 0.279727 0.231624

Close_Citi 0.344939 0.841156 0.356788 0.252684

JPM_Close 0.279727 0.356788 0.382494 0.223740

GS_Close 0.231624 0.252684 0.223740 0.244539}

df3.head()

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | NaN | NaN | NaN | NaN |

| 2007-04-01 | 0.354677 | -0.344488 | 0.249323 | -0.936011 |

| 2007-05-01 | -1.290186 | -0.528084 | -0.833508 | 0.100526 |

| 2007-08-01 | 0.604153 | 0.509924 | 0.334239 | 2.323950 |

| 2007-09-01 | -0.233824 | -0.875756 | -0.417976 | 0.171652 |

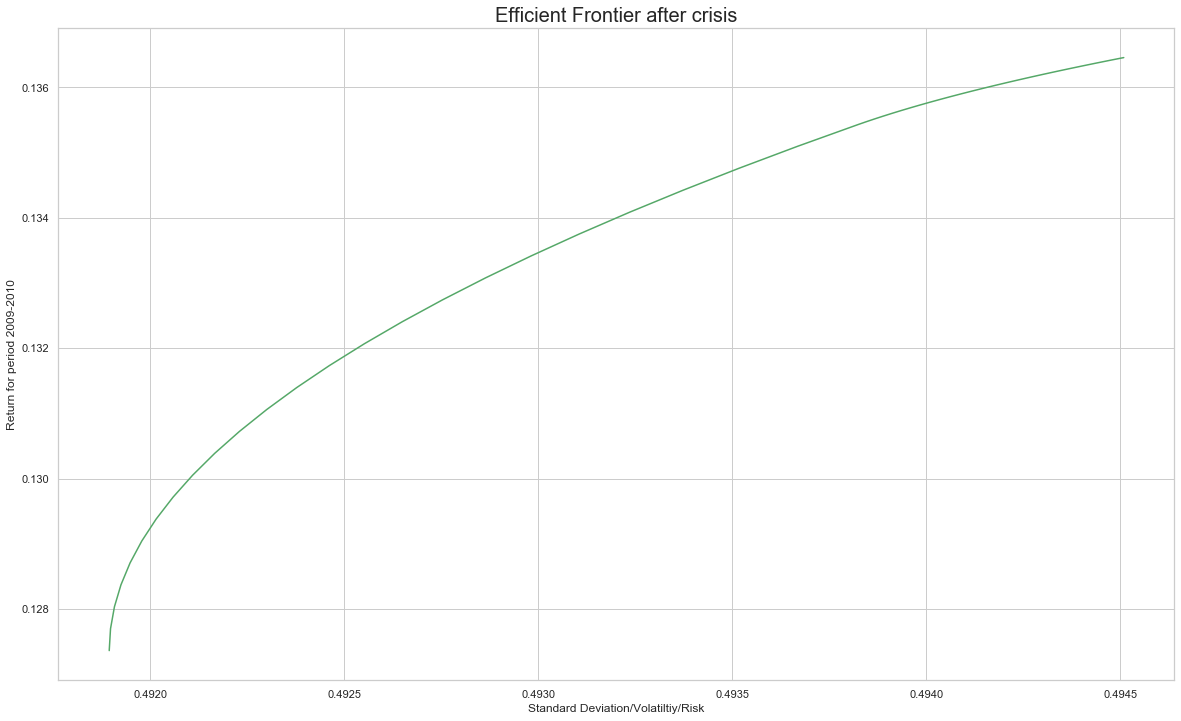

Great! The breakdown of the 2007 - 2010 period into sub-periods shows how the portfolio’s risk increased during the crisis , and this changed the risk-return trade-off after the crisis. For future reference, also note that although we used a loop in this exercise, a dictionary comprehension could also have been used to create the efficient covariance matrix.

# Create a dictionary of time periods (or 'epochs')

epochs = { 'during' : {'start': '1-1-2007', 'end': '31-12-2008'}}

# Compute the efficient covariance for each epoch

e_cov_during = {}

for x in epochs.keys():

sub_price = df4.loc[epochs[x]['start']:epochs[x]['end']]

e_cov_during[x] = CovarianceShrinkage(sub_price).ledoit_wolf()

# Display the efficient covariance matrices for all epochs

print("Efficient Covariance Matrices\n", e_cov_during)

Efficient Covariance Matrices

{'during': Close_MS Close_Citi JPM_Close GS_Close

Close_MS 0.994390 0.465336 0.298613 0.434874

Close_Citi 0.465336 0.713035 0.364848 0.323977

JPM_Close 0.298613 0.364848 0.422516 0.224668

GS_Close 0.434874 0.323977 0.224668 0.408773}

Efficient Frontier Using CLA Algorithm

Compute many efficient portfolios for different levels of risk efficient frontier: locus of (risk, return) pairs created by efficient portfolios PyPortfolioOpt library: optimized tools for MPT EfficientFrontier class: generates one optimal portfolio at a time Constrained Line Algorithm ( CLA ) class: generates the entire efficient frontier Requires covariance matrix of returns Requires proxy for expected future returns: mean historical returns

df4.head()

| Close_MS | Close_Citi | JPM_Close | GS_Close | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | 81.620003 | 552.500000 | 48.070000 | 200.720001 |

| 2007-04-01 | 81.910004 | 550.599976 | 48.189999 | 198.850006 |

| 2007-05-01 | 80.860001 | 547.700012 | 47.790001 | 199.050003 |

| 2007-08-01 | 81.349998 | 550.500000 | 47.950001 | 203.729996 |

| 2007-09-01 | 81.160004 | 545.700012 | 47.750000 | 204.080002 |

df3.head()

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | NaN | NaN | NaN | NaN |

| 2007-04-01 | 0.354677 | -0.344488 | 0.249323 | -0.936011 |

| 2007-05-01 | -1.290186 | -0.528084 | -0.833508 | 0.100526 |

| 2007-08-01 | 0.604153 | 0.509924 | 0.334239 | 2.323950 |

| 2007-09-01 | -0.233824 | -0.875756 | -0.417976 | 0.171652 |

df6=df3.loc['2007-03-01':'2008-12-31']

df7=df4.loc['2007-03-01':'2008-12-31']

e_cov_during = np.array(CovarianceShrinkage(df7).ledoit_wolf())

type(e_cov_during)

numpy.ndarray

returns_during = np.array(df6.mean())

efficient_portfolio_during = CLA(returns_during, e_cov_during)

print(efficient_portfolio_during.min_volatility())

{0: 0.0, 1: 0.0, 2: 0.4814250629859924, 3: 0.5185749370140076}

# Compute the efficient frontier

(ret, vol, weights) = efficient_portfolio_during.efficient_frontier()

plt.figure(figsize=(20,12))

plt.xlabel('Standard Deviation/Volatiltiy/Risk')

plt.ylabel('Return for period 2007-2008')

plt.title('Efficient Frontier during crisis',size=20)

plt.plot(vol,ret,c='r')

[<matplotlib.lines.Line2D at 0x27255455ac8>]

df9=df4.loc['2009-01-01':'2010-12-31'] # for covariance matrix (prices)

df10=df3.loc['2009-01-01':'2010-12-31'] # returns

returns_after = np.array(df10.mean())

print(returns_after)

[ 0.1059442 -0.06826069 0.05808973 0.13645525]

e_cov_after = np.array(CovarianceShrinkage(df9).ledoit_wolf())

efficient_portfolio_after = CLA(returns_after, e_cov_after)

(ret, vol, weights) = efficient_portfolio_after.efficient_frontier()

# Add the frontier to the plot showing the 'before' and 'after' frontiers

plt.figure(figsize=(20,12))

plt.xlabel('Standard Deviation/Volatiltiy/Risk')

plt.ylabel('Return for period 2009-2010')

plt.title('Efficient Frontier after crisis',size=20)

plt.plot(vol,ret,c='g')

[<matplotlib.lines.Line2D at 0x27255a9a5f8>]

## Risk reduced after crisis

Portfolio Optimization

df_returns = df1[['Return_MS','Return_Citi','Return_JPM','Return_GS']]

df_returns.head(10)

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Date | ||||

| 2007-03-01 | NaN | NaN | NaN | NaN |

| 2007-04-01 | 0.354677 | -0.344488 | 0.249323 | -0.936011 |

| 2007-05-01 | -1.290186 | -0.528084 | -0.833508 | 0.100526 |

| 2007-08-01 | 0.604153 | 0.509924 | 0.334239 | 2.323950 |

| 2007-09-01 | -0.233824 | -0.875756 | -0.417976 | 0.171652 |

| 2007-10-01 | 0.503898 | -0.809576 | 0.730307 | 1.955471 |

| 2007-11-01 | 0.975978 | 0.073873 | 0.435646 | 1.795331 |

| 2007-12-01 | 0.593112 | 0.386915 | -0.664590 | 0.990921 |

| 2007-01-16 | -0.302170 | 0.714620 | 0.830046 | -0.187104 |

| 2007-01-17 | -0.278810 | -0.696226 | 0.082630 | -0.168689 |

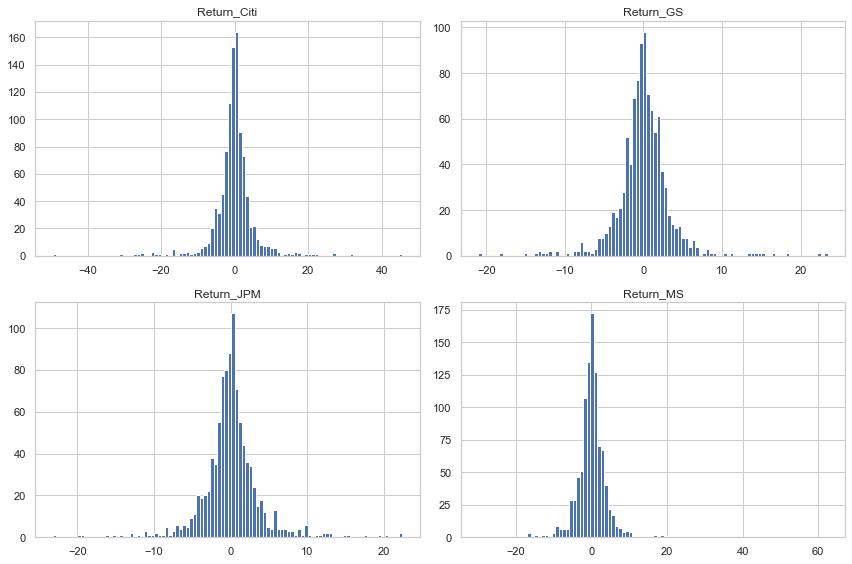

df_returns.hist(bins=100,figsize=(12,8))

plt.tight_layout()

df_returns.mean()

Return_MS -0.108756

Return_Citi -0.243700

Return_JPM -0.012875

Return_GS -0.017902

dtype: float64

df_returns.cov()*252

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Return_MS | 6322.118322 | 4271.390381 | 3127.726038 | 3508.654003 |

| Return_Citi | 4271.390381 | 7847.629460 | 3859.369779 | 3056.339857 |

| Return_JPM | 3127.726038 | 3859.369779 | 3766.313007 | 2435.835409 |

| Return_GS | 3508.654003 | 3056.339857 | 2435.835409 | 2984.295634 |

Portfolio Optimization using Monte Carlo Simulation (Random Weights)

np.random.seed(101)

print(df1.columns)

rand_weights = np.array(np.random.rand(4))

print('Random Weights : ',rand_weights)

## To make sum of random weights equal to 1 , divide each random generated weight by sum

print('Rebalance')

weights = rand_weights/np.sum(rand_weights)

print(weights)

Index(['Close_MS', 'Close_Citi', 'JPM_Close', 'GS_Close', 'Return_MS',

'Return_Citi', 'Return_JPM', 'Return_GS'],

dtype='object')

Random Weights : [0.51639863 0.57066759 0.02847423 0.17152166]

Rebalance

[0.40122278 0.44338777 0.02212343 0.13326603]

## Yearly portfolio expected return

exp_ret = np.sum(df_returns.mean()*weights*252)

exp_ret

-38.898628588158786

## Portfolio Volatility Yearly

exp_vol = np.sqrt(np.dot(weights.T,np.dot(df_returns.cov()*252,weights)))

exp_vol

70.83152895453853

## Sharpe Ratio

sr = exp_ret/exp_vol

print('Sharpe Ratio :',sr)

Sharpe Ratio : -0.5491710988354481

## Final code for monte carlo

np.random.seed(101)

num_ports = 10000

all_weights = np.zeros((num_ports,len(df_returns.columns)))

ret_arr = np.zeros(num_ports)

vol_arr = np.zeros(num_ports)

sharpe_arr = np.zeros(num_ports)

for ind in range(num_ports):

rand_weights = np.array(np.random.rand(4))

## To make sum of random weights equal to 1 , divide each random generated weight by sum

weights = rand_weights/np.sum(rand_weights)

all_weights[ind,:] = weights

## Yearly portfolio expected return

ret_arr[ind] = np.sum(df_returns.mean()*weights*252)

## Portfolio Volatility Yearly

vol_arr[ind] = np.sqrt(np.dot(weights.T,np.dot(df_returns.cov()*252,weights)))

## Sharpe Ratio

sharpe_arr[ind] = ret_arr[ind]/vol_arr[ind]

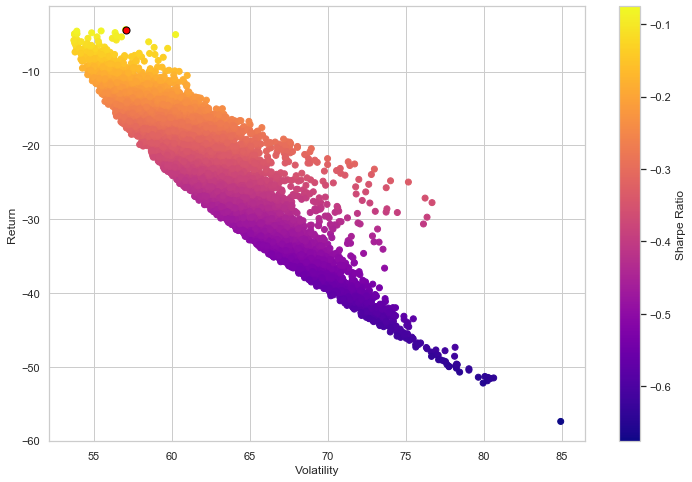

sharpe_arr.max()

sharpe_arr.argmax()

7872

all_weights[7872,:]

array([0.01225268, 0.00812669, 0.74934034, 0.2302803 ])

max_sr_ret = ret_arr[7872]

max_sr_vol = vol_arr[7872]

plt.figure(figsize=(12,8))

plt.scatter(vol_arr,ret_arr,c=sharpe_arr,cmap='plasma')

plt.colorbar(label='Sharpe Ratio')

plt.xlabel('Volatility')

plt.ylabel('Return')

plt.scatter(max_sr_vol,max_sr_ret,c='red',s=50,edgecolors='black')

<matplotlib.collections.PathCollection at 0x27253fcd630>

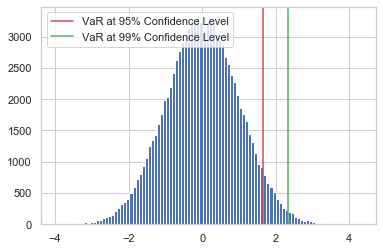

Var(Value at Risk) of a Normal Distribution

# Var of a Normal Distribution

# Create the VaR measure at the 95% confidence level using norm.ppf()

VaR_95 = norm.ppf(0.95)

# Create the VaR meaasure at the 5% significance level using numpy.quantile()

draws = norm.rvs(size = 100000)

VaR_99 = np.quantile(draws, 0.99)

# Compare the 95% and 99% VaR

print("95% VaR: ", VaR_95, "; 99% VaR: ", VaR_99)

# Plot the normal distribution histogram and 95% VaR measure

plt.hist(draws, bins = 100)

plt.axvline(x = VaR_95, c='r', label = "VaR at 95% Confidence Level")

plt.axvline(x = VaR_99, c='g', label = "VaR at 99% Confidence Level")

plt.legend(); plt.show()

95% VaR: 1.6448536269514722 ; 99% VaR: 2.317671064617457

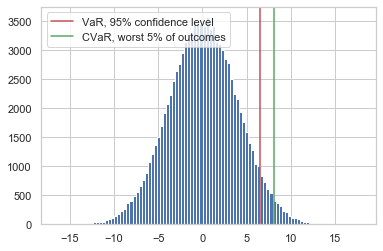

CVAR of a Normal Distribution

losses.head(10)

Date

2007-04-01 0.169125

2007-05-01 0.637813

2007-08-01 -0.943067

2007-09-01 0.338976

2007-10-01 -0.595025

2007-11-01 -0.820207

2007-12-01 -0.326589

2007-01-16 -0.263848

2007-01-17 0.265274

2007-01-18 0.922285

dtype: float64

mean_loss = losses.mean()

mean_loss

0.09580838926126413

std_loss = losses.std()

std_loss

3.903568122449752

# Compute the mean and variance of the portfolio losses

pm = mean_loss

ps = std_loss

# Compute the 95% VaR using the .ppf()

VaR_95 = norm.ppf(0.95, loc = pm, scale = ps)

# Compute the expected tail loss and the CVaR in the worst 5% of cases

tail_loss = norm.expect(lambda x: x, loc = pm, scale = ps, lb = VaR_95)

CVaR_95 = (1 / (1 - 0.95)) * tail_loss

# Plot the normal distribution histogram and add lines for the VaR and CVaR

plt.hist(norm.rvs(size = 100000, loc = pm, scale = ps), bins = 100)

plt.axvline(x = VaR_95, c='r', label = "VaR, 95% confidence level")

plt.axvline(x = CVaR_95, c='g', label = "CVaR, worst 5% of outcomes")

plt.legend(); plt.show()

VaR of Student’s t-distribution

from scipy.stats import t

mu = losses.rolling(30).mean()

sigma = losses.rolling(30).std()

mu

Date

2007-04-01 NaN

2007-05-01 NaN

2007-08-01 NaN

2007-09-01 NaN

2007-10-01 NaN

...

2010-12-23 -0.105515

2010-12-27 -0.175961

2010-12-28 -0.233157

2010-12-29 -0.170770

2010-12-30 -0.219959

Length: 1006, dtype: float64

sigma

Date

2007-04-01 NaN

2007-05-01 NaN

2007-08-01 NaN

2007-09-01 NaN

2007-10-01 NaN

...

2010-12-23 1.425831

2010-12-27 1.428301

2010-12-28 1.386096

2010-12-29 1.388099

2010-12-30 1.350370

Length: 1006, dtype: float64

rolling_parameters = [(29, mu[i], s) for i,s in enumerate(sigma)]

VaR_99 = np.array( [ t.ppf(0.99, *params)

for params in rolling_parameters ] )

# Fit the Student's t distribution to crisis losses

p = t.fit(losses)

# Compute the VaR_99 for the fitted distribution

VaR_99 = t.ppf(0.99, *p)

# Use the fitted parameters and VaR_99 to compute CVaR_99

tail_loss = t.expect( lambda y: y, args = (p[0],), loc = p[1], scale = p[2], lb = VaR_99 )

CVaR_99 = (1 / (1 - 0.99)) * tail_loss

print(CVaR_99)

26.276295920436993

26% Loss (CVaR) on a given portfolio investment during financial crisis

Parametric Estimation VaR

Parameter estimation is the strongest method of VaR estimation because it assumes that the loss distribution class is known. Parameters are estimated to fit data to this distribution, and statistical inference is then made.

Finding best parameters (Theta - Mean and SD) given portfolio data is called Parametric Estimation

In Parameter Estimation VaR, loss distribution is not given, thereby we fit different distribution and with the help of Anderson Darling test we check goodness of fit.

df.head(10)

| returns | |

|---|---|

| Date | |

| 2007-04-01 | -0.169125 |

| 2007-05-01 | -0.637813 |

| 2007-08-01 | 0.943067 |

| 2007-09-01 | -0.338976 |

| 2007-10-01 | 0.595025 |

| 2007-11-01 | 0.820207 |

| 2007-12-01 | 0.326589 |

| 2007-01-16 | 0.263848 |

| 2007-01-17 | -0.265274 |

| 2007-01-18 | -0.922285 |

df_returns = df.dropna(axis=0)

df_returns.head(3)

| returns | |

|---|---|

| Date | |

| 2007-04-01 | -0.169125 |

| 2007-05-01 | -0.637813 |

| 2007-08-01 | 0.943067 |

df_returns.describe()

| returns | |

|---|---|

| count | 1006.000000 |

| mean | -0.095808 |

| std | 3.903568 |

| min | -22.216434 |

| 25% | -1.501236 |

| 50% | -0.080673 |

| 75% | 1.319224 |

| max | 29.279192 |

params = norm.fit(losses)

params

(0.09580838926126402, 3.901627496865014)

VaR_95 = norm.ppf(0.95, *params)

print("VaR_95, Normal distribution: ", VaR_95)

VaR_95, Normal distribution: 6.513414528493276

print("Anderson-Darling test result: ", anderson(losses))

Anderson-Darling test result: AndersonResult(statistic=38.20183257088229, critical_values=array([0.574, 0.653, 0.784, 0.914, 1.088]), significance_level=array([15. , 10. , 5. , 2.5, 1. ]))

The Anderson-Darling test above value of 38.20 exceeds the 99% critical value of 1.088 by a large margin, indicating that the Normal distribution may be a poor choice to represent portfolio losses

## Null Hypothesis - No Skewness

# Test the data for skewness

print("Skewtest result: ", skewtest(losses))

Skewtest result: SkewtestResult(statistic=-6.655492127945391, pvalue=2.8235366881911988e-11)

# Fit the portfolio loss data to the skew-normal distribution

params = skewnorm.fit(losses)

# Compute the 95% VaR from the fitted distribution, using parameter estimates

VaR_95 = skewnorm.ppf(0.95, *params)

print("VaR_95 from skew-normal: ", VaR_95)

VaR_95 from skew-normal: 6.283943890895702

Losses are not normally distributed as the critical value exceeeds the 99% conidence interval of test statistic value Losses can be skewed

Definition wiki - anderson In many cases (but not all), you can determine a p value for the Anderson-Darling statistic and use that value to help you determine if the test is significant are not. Remember the p (“probability”) value is the probability of getting a result #that is more extreme if the null hypothesis is true. If the p value is low (e.g., <=0.05), you conclude that the data do not follow the normal distribution. Remember that you chose the significance level even though many people just use 0.05 the vast majority of the time. We will look at two different data sets and apply the Anderson-Darling test to both sets.

Note that although the VaR estimate for the Normal distribution from the previous exercise is larger than the skewed Normal distribution estimate, the Anderson-Darling and skewtest results show the Normal distribution estimates cannot be relied upon. Skewness matters for loss distributions, and parameter estimation is one way to quantify this important feature of the financial crisis.

Historical Simulation

EXAMPLE

#weights = [0.25, 0.25, 0.25, 0.25] #portfolio_returns = asset_returns.dot(weights) #losses = - portfolio_returns #VaR_95 = np.quantile(losses, 0.95)

Historical simulation: use past to predict future No distributional assumption required Data about previous losses become simulated losses for tomorrow

VaR_95_HS = np.quantile(losses,0.95)

print(VaR_95_HS)

5.245684561193499

## 5 % Loss with 95% confidence interval

Historical with monte carlo simulation VaR

# Initialize daily cumulative loss for the 4 assets, across N runs

N=10000

daily_loss = np.zeros((4,N))

returns.head()

| Return_MS | Return_Citi | Return_JPM | Return_GS | |

|---|---|---|---|---|

| Date | ||||

| 2007-04-01 | 0.354677 | -0.344488 | 0.249323 | -0.936011 |

| 2007-05-01 | -1.290186 | -0.528084 | -0.833508 | 0.100526 |

| 2007-08-01 | 0.604153 | 0.509924 | 0.334239 | 2.323950 |

| 2007-09-01 | -0.233824 | -0.875756 | -0.417976 | 0.171652 |

| 2007-10-01 | 0.503898 | -0.809576 | 0.730307 | 1.955471 |

mu = np.array([returns['Return_MS'].mean(),returns['Return_Citi'].mean(),returns['Return_JPM'].mean(),

returns['Return_GS'].mean()])

mu

array([-0.1087564 , -0.24369987, -0.01287549, -0.0179018 ])

mu = np.array([[-0.1087564],

[-0.24369987],

[-0.01287549],

[-0.0179018]])

type(mu)

numpy.ndarray

e_cov = returns.cov()

e_cov_1 = np.array(e_cov)

e_cov_1

array([[25.08777112, 16.94996183, 12.41161126, 13.92323017],

[16.94996183, 31.14138675, 15.31495944, 12.12833277],

[12.41161126, 15.31495944, 14.94568654, 9.66601353],

[13.92323017, 12.12833277, 9.66601353, 11.84244299]])

total_steps = 1440

# Create the Monte Carlo simulations for N runs

for n in range(N):

# Compute simulated path of length total_steps for correlated returns

correlated_randomness = e_cov @ norm.rvs(size = (4,total_steps))

# Adjust simulated path by total_steps and mean of portfolio losses

steps = 1/total_steps

minute_losses = mu * steps + correlated_randomness * np.sqrt(steps)

daily_loss[:, n] = minute_losses.sum(axis=1)

losses = weights @ daily_loss

print("Monte Carlo VaR_95 estimate: ", np.quantile(losses, 0.95))

Ordinary Least Square Ordinary least squares (OLS) regression is a statistical method of analysis that estimates the relationship between one or more independent variables and a dependent variable; the method estimates the relationship by minimizing the sum of the squares in the difference between the observed and predicted values of the dependent variable configured as a straight line.

Structural Breaks - Theory

Chow Test = Whether or not a structural break has occured in the data Visualization cannot determine exact structural break in the data Alternative - Time of structural break concides with time of increasing volatility Stochastic Volatility Model : Volatility can be analyzed statistically through the random probability distribution but cannot be predicted precisely

To check if the volatility is non stationary rolling window volatility is calculated

VaR and CVaR estimates that data distribution is same throughout (Stationarity Assumption) but there are structural breaks in between.

So Assume specific points in time for change Break up data into sub-periods Within each sub-period, assume stationarity

Chow TEST: Test for evidence of structural breaks 1. Null hypothesis - No break 2. Requires three OLS regressions 3. Regression for entire period 4. Two regressions, before and after break 5. Collect sum-of-squared residuals 6. Test statistic is distributed according to “F” distribution

Noe sometimes it is not easy to visualize the losses to detect the structural break Sometimes we can use Rolling window volatility to visualize the rolling volatity in the given time period

std() calculates a single value of volatility rolling.std calculates rolling volatility and you can plot and see the structural break

Backtesting Backtesting is the process of applying a trading strategy or analytical method to historical data to see how accurately the strategy or method would have predicted actual results.